Contact

ContactDecember FOMC

An Early Gift

December 21, 2023

Executive Summary:

- Markets responded with euphoria as Chair Powell signaled the end of the Federal Reserve’s (Fed) hiking cycle.

- To start, the Committee’s Summary of Economic Projections (SEP) implied a more dovish rate path than markets anticipated.

- Chair Powell followed up with a few answers detailing the Committee’s discussion of the appropriate time for rate cuts, a notable shift from prior communication where the skew was to additional hikes rather than cuts.

- Markets are pricing nearly a full cut by March of 2024 with an additional 5 by year-end. An everything rally has ensued, and little stands in its way through year-end.

- Ahead of the meeting, inflation stagnated near the prior month’s level. However, it was not enough to dissuade the Committee from shifting towards rate cuts.

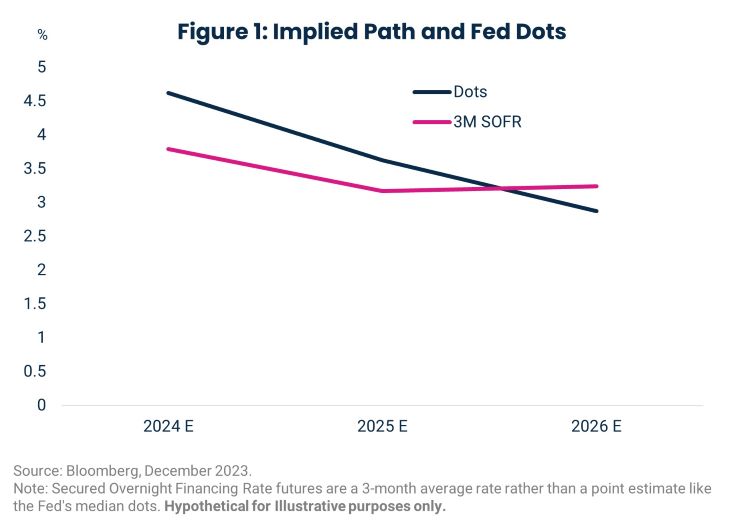

The response to the Federal Open Market Committee (FOMC) meeting occurred in two stages mirroring the areas of surprise. First, the median SEP dot for 2024 implied three cuts rather than the two that markets expected, implying a year-end rate around 4.6%. Further out, the cumulative number of cuts through year-end 2025 remained the same as did the terminal rate in 2026. However, the distribution of forecasts narrowed considerably with Committee members coalescing around a 3% rate by 2026. Combined with the economic forecasts, the Committee appears to doubt the likelihood of sustainably higher rates.

During the press conference, Powell revealed that the Committee is discussing the next question: when to begin cutting interest rates. It was in the context of the Committee remaining committed to doing what is necessary and not declaring victory prematurely, but the only thing that mattered to us was Powell opening the door to cuts. On inflation, Chair Powell described steady progress on all fronts and noted that cuts, on principle, should precede a return to 2 percent inflation as policy remains restrictive. This another notable shift from a focus on current progress to more emphasis on forecasted progress.

The market response to Powell was clear as well. A falling discount rate lifted nearly all asset prices. Anything that was particularly sensitive to higher interest rates, areas like banks, small-caps, or unprofitable companies outperformed significantly. Similarly, factor performance reversed with value and volatility doing well, while quality, size, and profitability underperformed. It is difficult to tease out how much of the relative performance is mean reversion versus a durable shift for 2024. Pricing 6 cuts in 2024 is premature given inflation above 3 percent. However, in the short-term, there are few obstacles to year-end to further mean reversion or pricing more cuts than the Fed’s baseline.

Stagnant, But Not Worrying Inflation

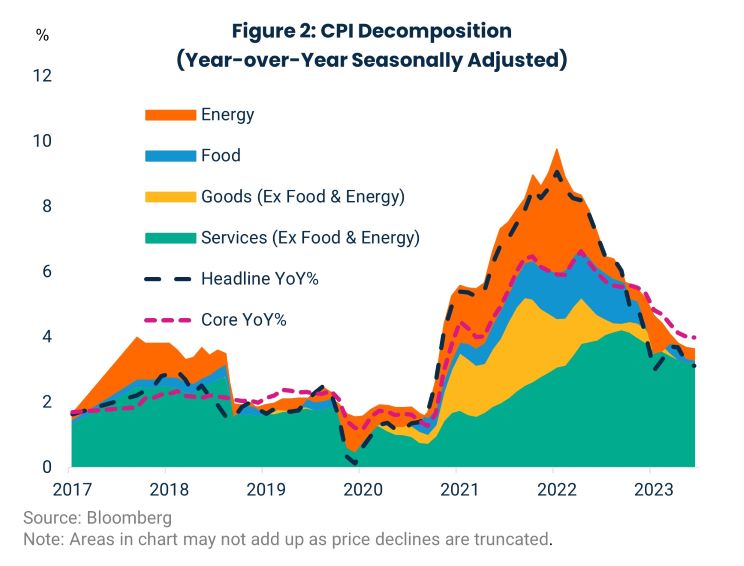

Headline and core inflation stagnated at 3.1 and 4 percent year-over-year, respectively. Energy prices continued to weigh on headline inflation as prices at the pump declined further as global crude supply surprised to the upside. Within core, goods prices declined for the 6th consecutive month amid weakness in apparel and furniture prices, confirming data that showed a steep increase in holiday discounting over the Thanksgiving sales period. The data around Black Friday sales is clouded by the secular shift from brick and mortar to ecommerce channels, but the CPI data leans against the idea of a profit surge for retailers in November. Core goods prices are likely to remain in deflation for some time absent a material reacceleration in economic growth.

Services, the Fed’s focus, firmed as shelter prices ticked up. Disinflation in the cost of shelter continues to be bumpy, but the direction of travel is still lower. Marginal rental prices are settling near pre-COVID levels as the single-family home deficit offsets the significant increase in multi-family supply. Elsewhere, medical services jumped as expected given the annual update in insurers’ retained profits, a reversal of a consistent source of disinflation over the past year. The 0.5% increase in core services, excluding shelter, remains at an uncomfortably high level for the Fed, but, as today’s meeting made clear, not enough to dissuade them from ending the hiking cycle.

For more information, please access our website at www.harborcapital.com or contact us at 1-866-3135549.

Important Information

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. The information provided in this presentation is for informational purposes only.

This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy.

Forecast and estimates are based on hypothetical assumptions and for informational purposes only. This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy. The information presented does not represent the results that any particular investor may actually attain. Actual results will differ, and may differ substantially, from the hypothetical information provided.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

Harbor Capital Advisors, Inc.

3296313