Contact

ContactNovember FOMC: Shifting the Balance

November 06, 2023

Executive Summary:

- With rates on hold, the Committee may be ready to call it quits on hiking as inflation concerns begin to give way to concerns about overdoing it.

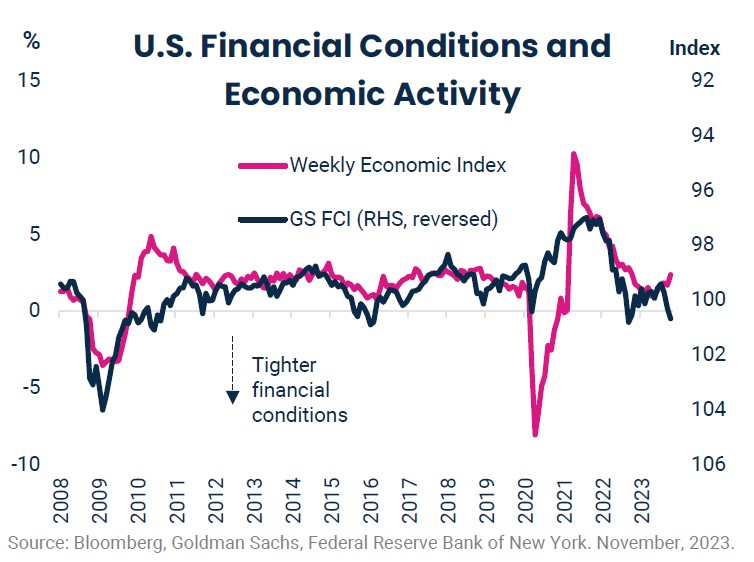

- The statement changes were minimal as the Committee acknowledged the blockbuster Q3 Gross Domestic Product (GDP) print and the tightening in financial conditions stemming from higher interest rates and lower equity indices since the last meeting.

- During the press conference, Chair Powell was optimistic about the source of recent economic strength stressing an unwind to the pandemic shocks and positive labor supply developments stemming from the robust economy and immigration.

- The net result of the meeting was an easing in financial conditions as markets reacted positively to the prospect of no more hikes despite a resilient economy.

- Predicting the market’s reaction to any Federal Open Market Committee (FOMC) meeting is difficult, but too large an easing in financial conditions in the next few weeks could force the Committee into a December hike.

Starting with the statement, the FOMC upgraded their assessment of growth as they marked-to-market after last week’s 4.9% GDP print. Similarly, the committee acknowledged the tightening in financial conditions stemming from the increase in long-term interest rates. Both changes acknowledge the world in front of them but should not be read as a signal of the world ahead. Without a new Summary of Economic projections to refer to, Chair Powell was left to describe how the Committee’s forecast evolved since September. In a sentence, the uptick in inflation last month did not dissuade the Committee that disinflation and a soft landing remain on track.

Powell’s comments were instructive for the Committee’s evolving view of the labor force and how it feeds into their inflation forecast. In both his opening statement and in several answers subsequently, Powell described how the U.S. labor market is undergoing a positive labor supply shock as both immigration and prime-age labor force participation rebound above pre-pandemic levels. A larger supply of labor is resulting in slower wage gains as businesses compete less aggressively for workers. And with supply driving the normalization of the labor market, Powell noted that the potential growth rate for the U.S. could be above 2 percent, a nod to the sustainability of current interest rates. If the Committee is right, the soft-landing in the mid-90s may be the best analogue for the current period. At that time, a positive productivity shock stemming from the adoption of the internet offset the Federal Reserve’s tightening without pushing prices higher.

The risk to the FOMC of this forecast was evident in the Chair’s first answer. Financial conditions are a difficult target for the Committee to measure the policy stance against as market expectations are constantly evolving in response. Powell said that the Committee is not confident that financial conditions are tight enough to achieve its goals. The rest of the press conference undermined that point as Powell focused on the limited costs of disinflation so far leaving financial conditions much easier than Tuesday. The FOMC attempts to forecast how the market will respond to their communications, so over the next few weeks we will have a better sense of whether the Committee’s intended message matched the response in asset prices. Our view is that the Chair’s remarks skewed more optimistic than intended, but a further easing in financial conditions is required before the Committee takes steps to talk up the possibility of a December rate hike.

Where does it leave our positioning? Our regime indicators place us right in the middle of the road. Growth was elevated in the third quarter; meanwhile leading indicators suggest weaker growth ahead. This gap has been a consistent feature of 2023, which tempers our desire to lean too far into our qualitative view that the probability of a recession as reflected in market prices remains too low. As a result, we are sticking close to a neutral stance while leaning into beneficiaries of a cyclical rebound in the equity market like the energy sector without sacrificing our ability to diversify in a drawdown through an allocation to gold.

For more information, please access our website at www.harborcapital.com or contact us at 1-866-313-5549.

Important Information

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. The information provided in this presentation is for informational purposes only.

This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

3212417