Contact

ContactAsset Allocation Viewpoints & Positioning Q3 2022

October 26, 2022

Macro Landscape

“It’s the Economy, Stupid”

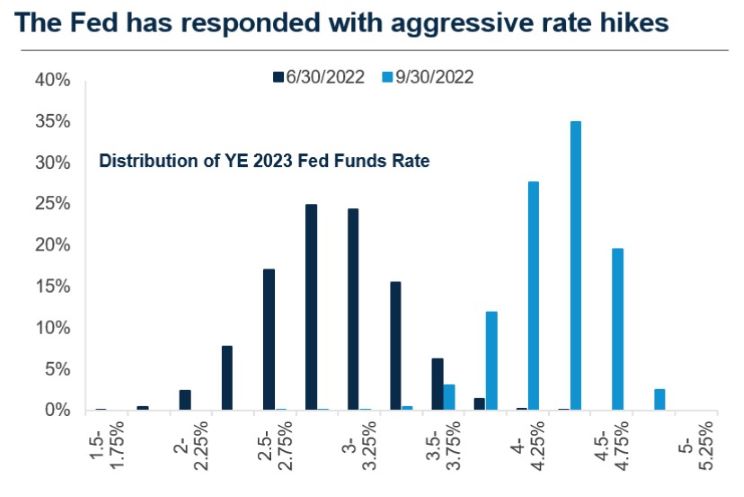

- The Federal Reserve continues to quickly hike interest rates to “get ahead of the curve” as core inflation has shown few signs of moderating. The Fed is focused on backward looking indicators, such as the labor market and inflation, as guideposts for monetary policy. Markets are therefore calling the expansion into question, and we would agree. The likelihood of recession is high and our base case for 2023.

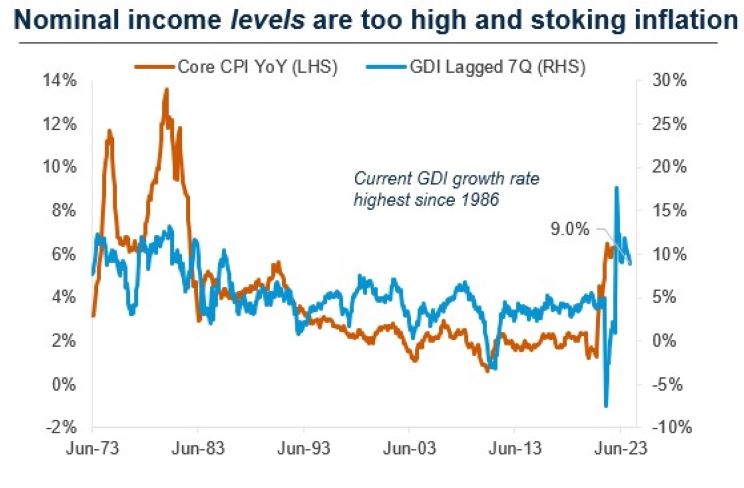

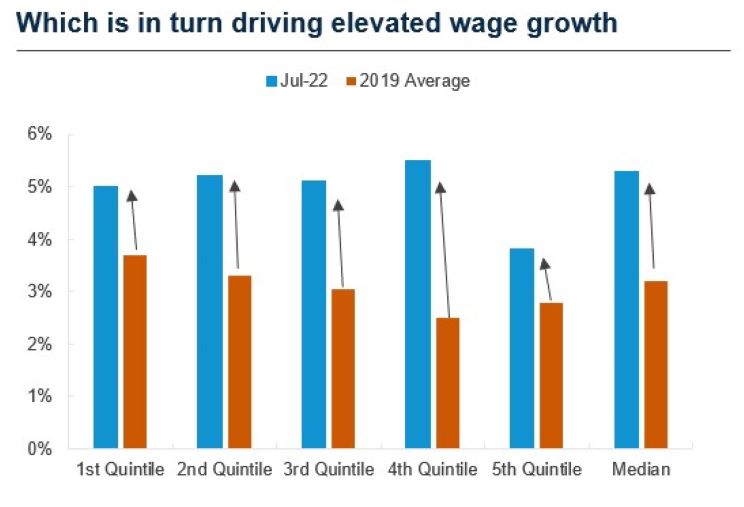

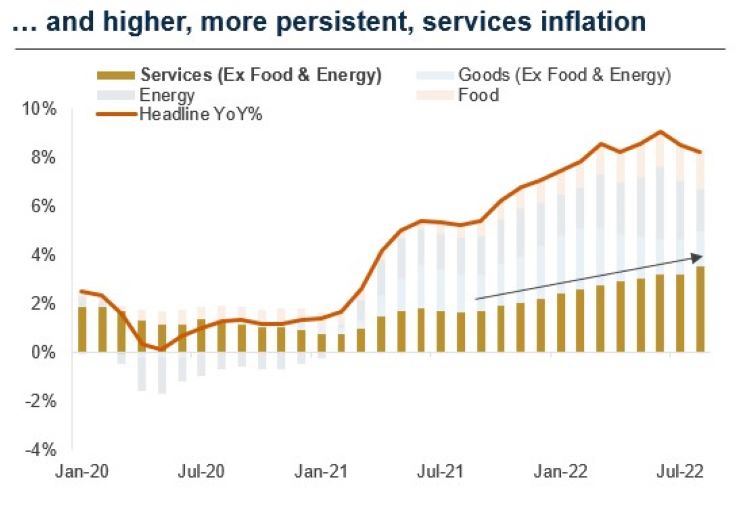

- Nominal income growth remains far too strong, currently running around 9.0%, and continues to keep underlying inflation elevated relative to target. We believe that the remedy is a meaningful softening in the labor market which will be accompanied by a rise in the unemployment rate. This has typically coincided with a recession.

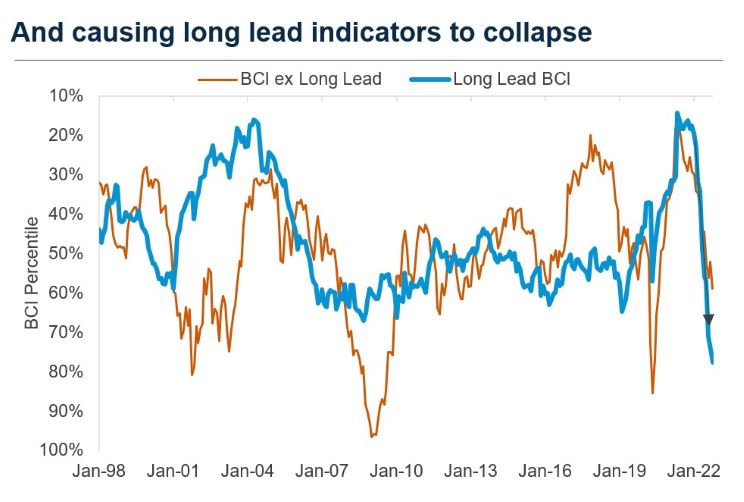

- While the Fed is focused on lagging indicators such as wage growth, the unemployment rate and services inflation, we are focused on leading indicators which are flashing red. Historically, the gap between weak leading indicators and strong lagging indicators is closed only one way - lagging indicators eventually succumb to the cycle.

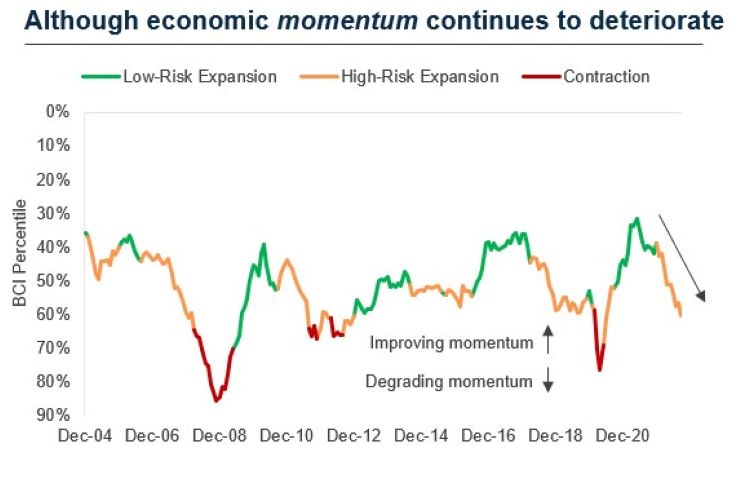

- Inflationary bear markets bottom when growth bottoms, not when inflation peaks. Although inflation appears to have peaked on a yearly growth rate basis, we do not see growth momentum bottoming until 2Q 2023 at the earliest.

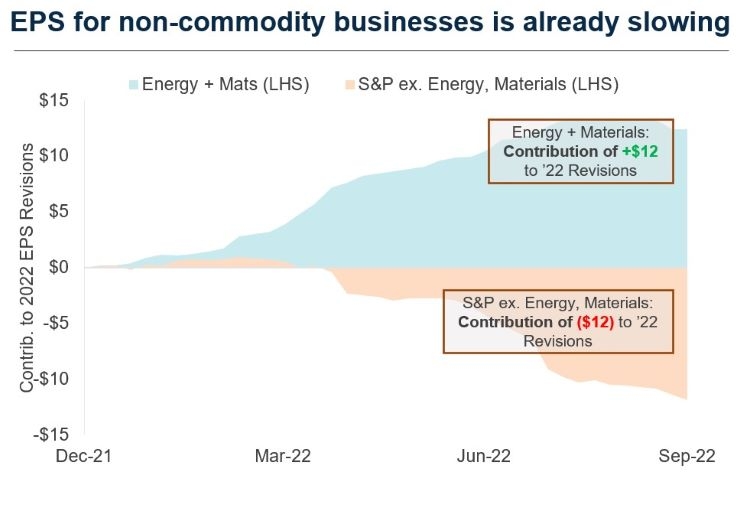

- Corporate earnings are far above trend growth and historically fall from these levels. We do not think this cycle will be any different; the Fed will see to that.

- We see two scenarios as most likely in the next 12 months: 1) inflation comes down to target as policy tightening has been sufficient to cause a recession (interest rates fall and cash flows fall), or 2) inflation does not come down to target as policy tightening has been insufficient to cause an acute growth slowdown, and therefore policy will tighten further than what is priced (rates rise further and cash flows do not fall, yet). We believe that both scenarios are very negative for risk assets.

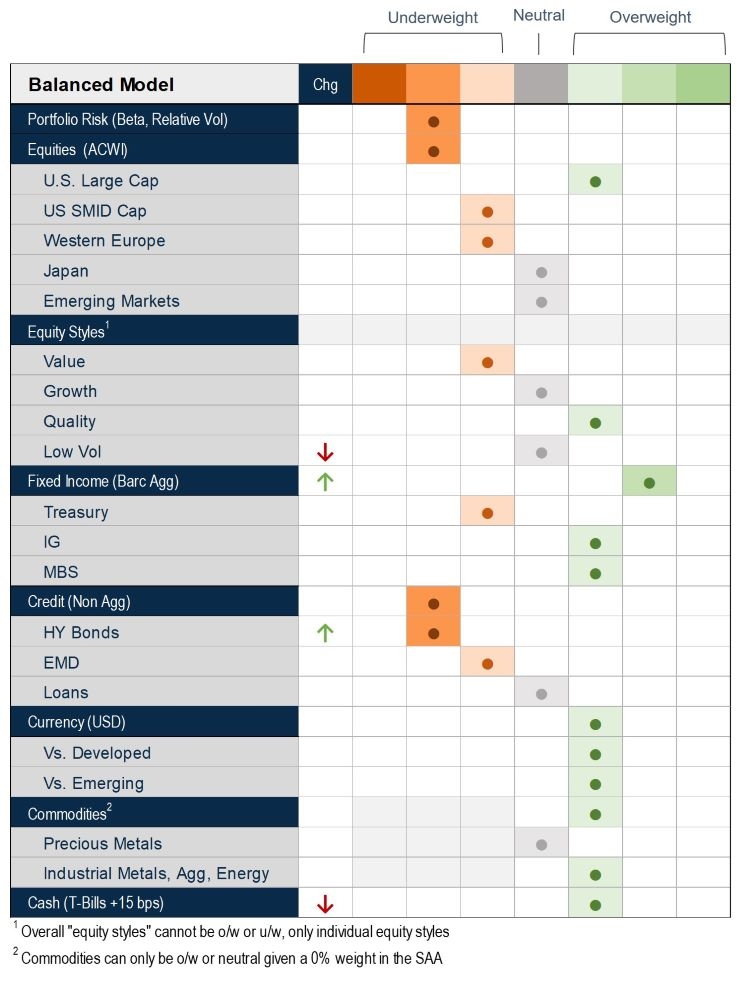

Asset Allocation Action Items:

- Retain equity underweight, model outcome is recession

- Reduce low vol exposure given stretched valuation

- Increase core fixed income exposure primarily through moderate duration investment grade

- Reduce underweight to high yield given attractive yield levels and preference to underweight equities

Source: Harbor MAST; Positioning as of September 2022

Equity Markets

We went further underweight equities in August. Despite the significant derating of equities year-to-date, we maintain our underweight as we expect the next phase of this cycle to result in an acute growth slowdown, corresponding downward earnings revisions, and widening of the equity risk premia. We maintain our relative overweight exposure to quality sectors such as Healthcare, which we expect to be more resilient to broad macroeconomic headwinds; we have also reduced our exposure to the Low Volatility style given unattractive valuations, and therefore reduced positive convexity if a downturn manifests.

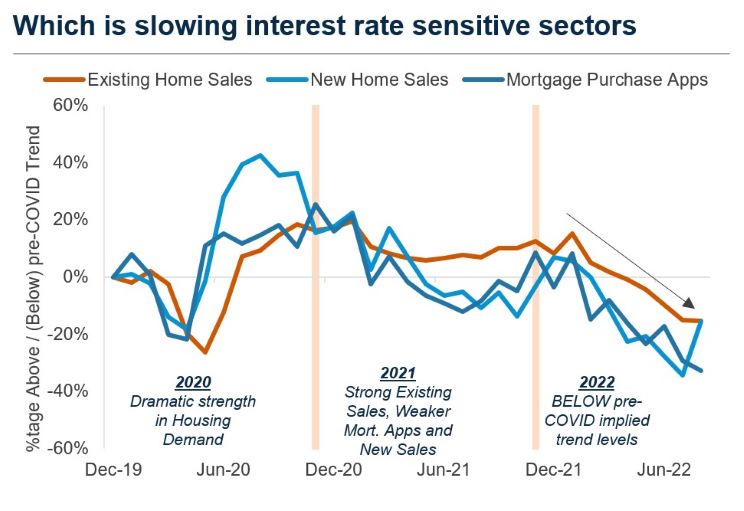

We are beginning to see the effect of tighter financial conditions engineered by global central banks on growth momentum. The first phase of the equity drawdown has consisted of equity multiples derating due to rising interest rates. The second and third phases will, in our view, result in rising risk premia and headwinds to corporate fundamentals. As a result, we further reduced our overall equity exposure and are continuously wary of European exposures due to the risk of an energy crisis. We are modestly overweight large-cap relative to small-cap. We continue to favor sectors with predictable and resilient profits.

The risk of a recession over the next twelve months is high. There remains a path to a soft landing, but our expected outcome is a recession in the middle to second half of 2023. We think risks to the global economy are tilted to the downside, with additional exogenous risk from significant geopolitical tension.

Fixed Income

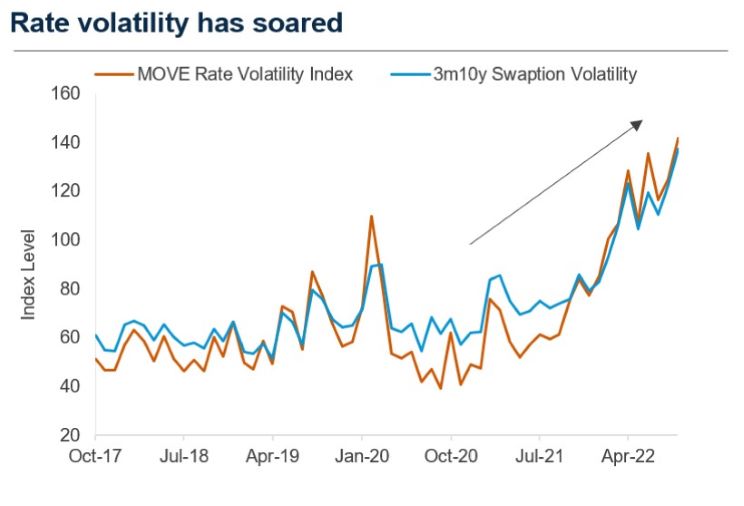

The FOMC's tacit acknowledgement that the modal outcome for 2023 is a recession increases our confidence that long-dated interest rates are more likely to be lower than higher in 12 months. However, the road ahead will remain volatile as central bank interest rate hikes combine with balance sheet reduction to create a highly uncertain environment for fixed income markets. We expect the curve to invert further as the FOMC keeps its policy rate elevated in 2023, meanwhile markets will price in eventual rate cuts and falling inflation as the U.S. enters a recession. Directional bets aside, the yields across fixed income provide an appealing alternative to equities for the first time in a while.

Credit Markets

Despite the widening in spreads year-to-date, we think there is further to go as corporate credit strains have yet to emerge. We think the forthcoming default cycle will be negligible for investment grade securities and prefer high-rated exposures.

Key Macro Views and Portfolio Implications

- We remain confident that the Fed will do what is necessary to reign inflation in, even if that means causing a recession.

- Although we are not certain if there has been sufficient tightening in financial conditions to slow aggregate demand and raise the unemployment rate, we are confident that it is inevitable.

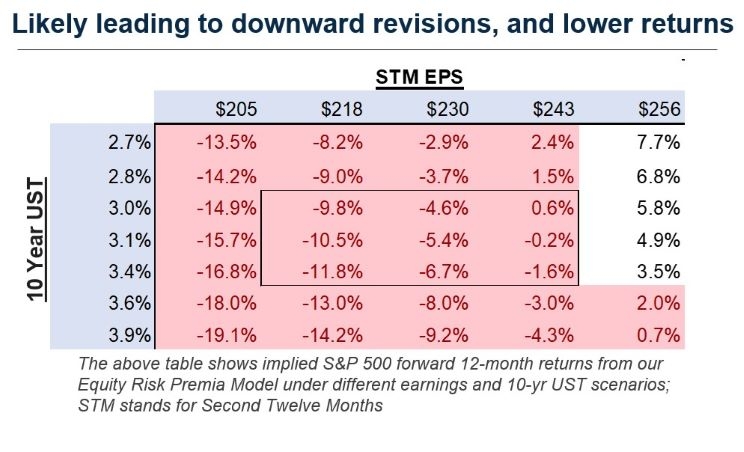

- If more policy tightening is required, interest rates will rise further and multiples will fall. If more policy tightening is not required, an acute growth slowdown is on the horizon and cash flows will fall. Either way, equities and credit look set to decline further.

- At current yield levels, we prefer core fixed income to risk assets such as equities and credit. Investment grade bonds now offer a very attractive yield with negligible default risk. Although interest rates may rise further in the coming months, we are confident that they will fall over the next 12 months as a recession likely unfolds.

- We prefer to allocate more of our risk budget to an equity underweight rather than high yield at this stage. If it takes 9 to 12 months for a recession to materialize, we would rather collect the attractive carry of HY bonds than own equities. We continue to dislike HY bonds in an absolute sense as spreads are biased wider from here as default rates inevitably tick higher.

- Although Europe looks very cheap on a near-term multiple basis, our analysis of Europe’s equity risk premia taking into account the region’s low ROE paints a less attractive picture. Further, we believe Europe’s “cheapness” is a bit of a mirage as the region will look less cheap once earnings fall due to the combination of financial conditions tightening and the energy crisis.

- We believe energy prices may rise over the next 3 to 6 months as US Strategic Petroleum Reserve (SPR) releases go away, new European sanctions on Russia take effect in December, OPEC+ cuts supply, and potential demand upside from China if zero-Covid restrictions are ultimately softened. Higher gasoline prices increase the odds of a recession as real consumption falls and inflation expectations rise.

Asset Allocation Views: The Bottom Line

Source for all charts: Harbor MAST, Bloomberg L.P., CME FedWatch, Factset; Data as of September 2022

Important Information

The views expressed herein are those of the Harbor Multi Asset Solutions Team at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. These views are not necessarily those of the Harbor Investment Team and should not be construed as such. The information provided is for informational purposes only.

Past performance is no guarantee of future results.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

All investments are subject to market risk, including the possible loss of principal. Stock prices can fall because of weakness in the broad market, a particular industry, or specific holdings. Bonds may decline in response to rising interest rates, a credit rating downgrade or failure of the issue to make timely payments of interest or principal. International investments can be riskier than U.S. investments due to the adverse affects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. These risks are generally greater for investments in emerging markets. Fixed income securities fluctuate in price in response to various factors, including changes in interest rates, changes in market conditions and issuer-specific events, and the value of an investment may go down. This means potential to lose money. As interest rates rise, the values of fixed income securities are likely to decrease and reduce the value of a portfolio. Securities with longer durations tend to be more sensitive to changes in interest rates and are usually more volatile than securities with shorter durations. Interest rates in the U.S. are near historic lows, which may increase exposure to risks associated with rising rates. Additionally, rising interest rates may lead to increased redemptions, increased volatility and decreased liquidity in the fixed income markets.

Certain forecasts, estimates and returns are based on hypothetical assumptions. It is for informational and illustrative purposes only. This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy. The forecasts, estimates and return presented do not represent the results that any particular investor may actually attain. Actual performance results will differ, and may differ substantially, from the hypothetical information provided.

Indices listed are unmanaged, and unless otherwise noted, do not reflect fees and expenses and are not available for direct investment.

2556768